Climate Change

Climate Risks and Opportunities

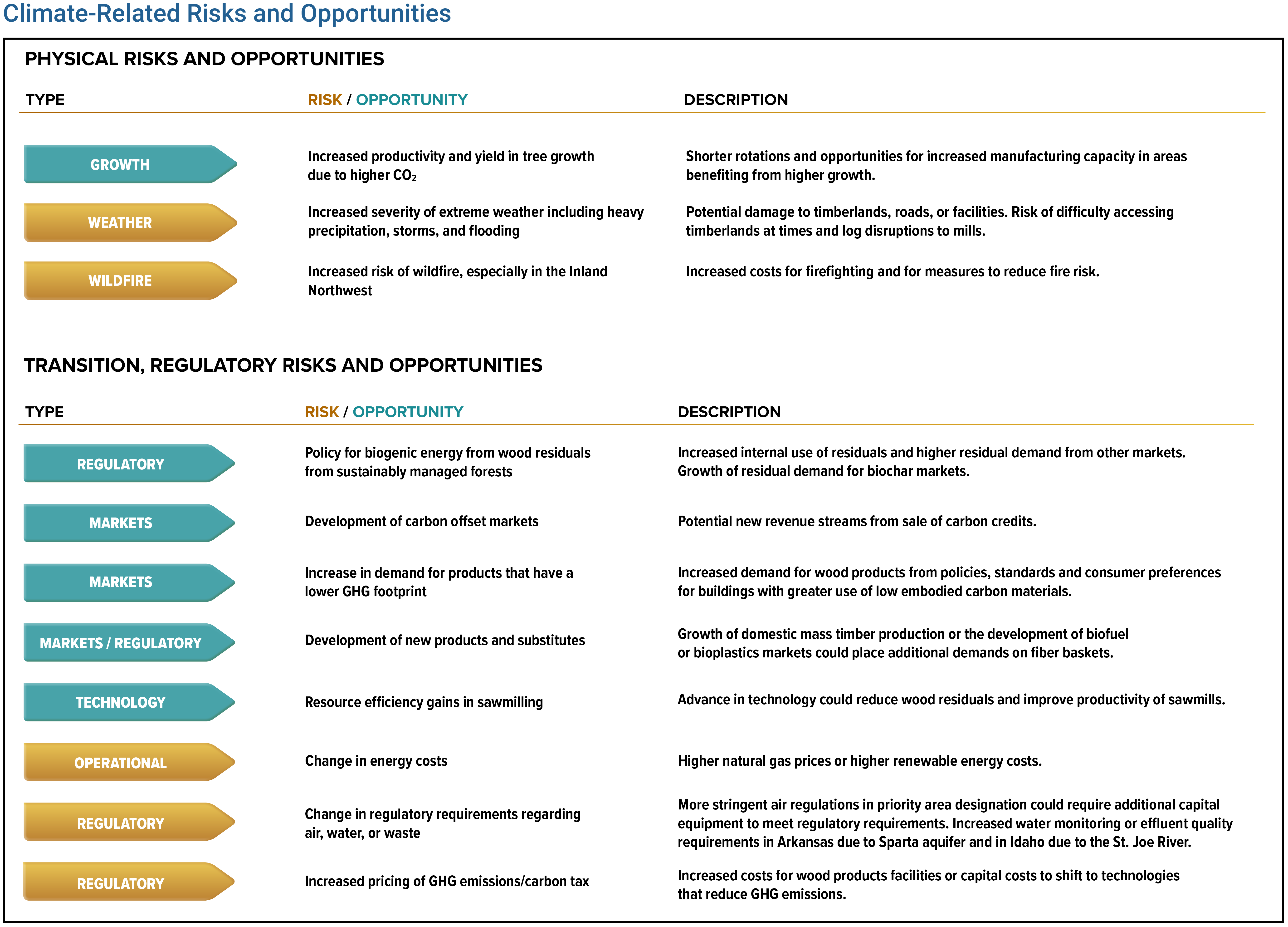

Climate change presents both risks and opportunities for PotlatchDeltic. The Board of Directors and the management team continue to expand their consideration of these risks and opportunities on Company strategy, operational decisions, risk management oversight, and performance.

PHYSICAL CLIMATE IMPACTS

PotlatchDeltic’s timberland climate analysis evaluates the potential physical impacts that changes in atmospheric CO2, temperature, and precipitation could have on our timberlands under various greenhouse gas (GHG) scenarios. We have evaluated potential physical impacts on four regions: 1) our Idaho timberlands; 2) our Gulf South timberlands; 3) our Southeast timberlands; and 4) our Lake States procurement region. The analysis was conducted utilizing guidance from the Task Force on Climate-related Financial Disclosures (TCFD) and using the National Council for Air and Stream Improvement (NCASI) Climate Projection Analysis Tool (NCASI Climate Tool).

The analysis is based on the Intergovernmental Panel on Climate Change (IPCC) scenarios called Representative Concentration Pathways (RCP). An RCP represents a prescribed pathway for anthropogenic (human caused) GHG emissions and land use change and serves as the basis for modeling the resulting atmospheric CO2 equivalent concentration. Concentrations project the resulting radiative forcing or additional warming that could occur in the lower atmosphere under a given emission pathway.

Following TCFD guidance, we evaluated four RCPs or sets of potential future scenarios, including a highly unlikely, high consequence scenario: RCP 2.6, RCP 4.5, RCP 6.0, and RCP 8.5. The RCP 2.6 pathway assumes rapid reductions in emissions with broad global participation and would result in about 1.5°C to 2°C of warming by 2100 relative to pre-industrial levels. Warming occurs by decade 2040-2049 and no additional warming occurs through 2100. RCP 4.5 assumes emissions peak around 2080 and then remain level through 2100 with global temperature projected to rise 2.5°C to 3°C by 2100 relative to pre-industrial levels. RCP 6.0 stabilizes warming by 2100 by reducing GHG emissions and applying new technologies and would result in about 3°C to 3.5°C of warming by 2100 relative to pre-industrial levels with the higher warming occurring from 2060 to 2100. RCP 8.5 assumes little effort to reduce emissions resulting in a failure to curb radiative forcing by 2100 and would result in about 5°C rise in global temperature by 2100 relative to pre-industrial temperatures. We are including RCP 8.5 as a highly unlikely high consequence scenario since the probability of this scenario is broadly considered unplausible given the global climate policies and reduction initiatives already implemented.

The NCASI Climate Projection Analysis Tool (CPAT) utilizes spatially downscaled climate model projections from the Coupled Model Intercomparison Project (CMIP-5) dataset for the period 2000-2099 for the four RCP scenarios. The model projections include temperature and precipitation impacts to 2100 for our two identified regions and enable the evaluation of climate boundaries for our primary tree species in each region. In addition, we address the general biological response for timberlands arising from higher CO2 levels in the atmosphere. It is important to note that confidence in climate model output is greatest for global and continental-scale results. Downscaled models, currently, cannot reliably replicate climate histories at local to regional scales. This means that model outputs for any region may not be representative of actual future conditions.

Projections of future greenhouse gas concentrations and localized climatic conditions have many variables. The ability to integrate the variables at meaningful scales to predict forest growth is subject to substantial ranges of error that encompass the entire range of the projected outcomes. Our initial analysis of regional physical climate changes and the potential for positive and negative impacts has revealed as many or more upside impacts to tree growth and productivity as downside risks or losses. Overall, increased CO2 concentrations coupled with gradual warming and largely unchanged precipitation patterns are supportive of productive forests.

TRANSITIONAL CLIMATE IMPACTS

Climate-related transition risks and opportunities include changes in policy or regulatory requirements, technology-related requirements, and market changes. The risks identified are incorporated into our Enterprise Risk Management process, and we continue to enhance our mitigation measures. Opportunities are considered in our strategic and operating plans and in our advocacy and policy initiatives. These factors can impact our business, strategy, and financial planning.

Markets utilizing biomass sourced from sustainably managed forests could expand as new bio-based products emerge ranging from bioplastics to biofuel. These could expand market demand for fiber and for residual wood fiber remaining from wood product manufacturing, a portion of which otherwise could go to waste. Net-zero transition commitments combined with circularity-oriented policies could drive growth of these bio-based materials for end uses such as food packaging, consumer goods, or aviation fuels.

The emerging momentum for mass timber in tall buildings exemplifies how innovation in wood products can provide significant opportunities. Developers and architects are attracted to the ability to incorporate sustainability and the carbon capture benefits of mass timber, its advantages, and its aesthetic appeal in non-residential and multifamily buildings. The recent changes to the International Building Codes allow mass timber to be used to construct buildings that are up to eighteen stories and provide potential for significant growth of mass timber use. Other new technologies for products using cellulose or wood fiber also continue to be developed and could increase with incentives that promote their development. Policies and incentives that encourage greater use of wood-based products in buildings or in building materials are also expected to increase, including emphasis on green building certification programs. Buildings are responsible for 39% of global energy-related carbon emissions, of which 28% are from operational emissions and 11% are from materials and construction (embodied carbon). Incentives, such as a transferable tax credit, could be established for use of higher performing products in construction to lower the embodied carbon or CO2 equivalent emissions associated with a cradle-to-grave footprint. Federal procurement policies could also prioritize carbon beneficial building materials. Wood products are well positioned to benefit from such policies given that they store carbon and have lower embodied carbon emissions, when sourced from sustainably managed forests, relative to other substitute materials.

Carbon taxes could be introduced to set a price that emitters pay per ton of GHG emissions to encourage companies to reduce their emissions. Taxes could be based on emissions or be applied to specific GHG intensive products such as gasoline. Our GHG emissions are relatively low and are mostly from natural gas and electricity used at our wood products facilities and from mobile sources harvesting timber and hauling logs. A tax could increase costs associated with these operations or result in additional capital expenditures to shift to other technologies.

The development of emissions trading systems (cap-and-trade) could continue to expand through emissions caps across specific industries. This mechanism currently exists in California as a statewide multi-sector initiative. We currently participate in the California Air Resources Board Cap-and-Trade system, which limits the amount of greenhouse gases (GHG) industries can emit.

Market-based policy mechanisms that reward carbon benefits at scale have the potential to support a significant market opportunity for sustainably managed working forests. These could develop as a transferable landowner tax credit for carbon sequestration as well as through carbon offset programs. For example, frameworks could utilize a practice-based option where the tax credit or offset is determined by forest owner implementation of USDA practices based on science-based sequestration estimates. In addition, frameworks could also provide a performance-based option that would enable a tax credit or offset to be determined by carbon sequestration above a baseline using a credible carbon accounting framework that is rigorous and streamlined.

Voluntary offset markets for carbon emissions are likely to continue to grow as companies rely on offsetting projects to achieve GHG reduction targets by mitigating some of their emissions. As demand for carbon credits grows, voluntary markets that are large, transparent, and verifiable are developing. Regulatory landscapes and market frameworks are evolving, which could build confidence in the use of forest carbon offsets to support a company’s transition to net-zero. As demand increases, pricing for carbon offsets from sustainably managed forests are improving, resulting in viable options to establish an offset through afforestation, improved forest management practices, or delayed harvests.

Demand for carbon capture and storage (CCS) is expanding as a technology that can capture carbon dioxide emissions from industrial processes such as coal-fired power plants and store them underground. Market opportunities for CCS could result in favorable locations with suitable geological formations.

PotlatchDeltic is the largest private landowner in Idaho with approximately 626,000 acres of timberland in northern Idaho. Our average site index on the PotlatchDeltic Idaho timberlands is considerably higher than the average Inland Northwest due to better soils with a volcanic ash base, higher precipitation, and an ideal elevation.

LEARN MORE ABOUT IDAHO CLIMATE ANALYSIS

PotlatchDeltic owns nearly 1.2 million acres in the Gulf South region. We own nearly 950,000 acres of timberland in Arkansas, 118,000 acres in Mississippi, approximately 87,000 acres in Alabama, and 30,000 acres in Louisiana. We mainly grow southern yellow pine with a mix of red oak, white oak, and other hardwoods in bottomlands.

LEARN MORE ABOUT GULF SOUTH CLIMATE ANALYSIS

PotlatchDeltic owns approximately 278,000 acres of timberland in the Southeast. This includes approximately 215,000 acres in Georgia and approximately 63,000 acres in South Carolina. Over 86% of our upland stands in the area are dominated by loblolly pine with other conifer species such as slash and long-leaf pine also present. Riparian acreage is dominated by hardwoods such as oaks, yellow poplar, or sweetgum.

LEARN MORE ABOUT SOUTHEAST CLIMATE ANALYSIS

PotlatchDeltic owns two sawmills in the Lake States. The sawmills produce precision-cut studs from spruce, pine, and fir (SPF). The Gwinn, Michigan sawmill has 185 MMBF annual capacity and the Bemidji, Minnesota sawmill has 140 MMBF annual capacity. We do not own timberlands in the Lake States and both sawmills procure all their logs from external sources.

LEARN MORE ABOUT LAKE STATES CLIMATE ANALYSIS

In forest management, we often talk of genetically enriching a tree species, but what does that really mean? One thing it does NOT mean is that we plant genetically modified organisms (GMO). GMOs are created through splicing, separating, and adding distinct genetic material to a model organism using various molecular biology techniques.

LEARN MORE ABOUT GENETIC ENRICHMENT TREE SPECIES

Higher atmospheric CO2 concentration and atmospheric nitrogen deposition can lead to multiple effects from CO2 enrichment resulting in productivity gains for timberlands. In response to elevated CO2, trees use water more efficiently, which increases growth efficiency and reduces water loss.

LEARN MORE ABOUT TIMBERLAND PRODUCTIVITY IMPACTS